The Quiet Revolution: How Solo Aging Women in 2026 Navigate Systemic Challenges to Achieve Total Sovereignty

In 2026, a profound demographic shift is reshaping the landscape of aging, particularly for women. A "quiet revolution" is underway, driven by a generation of women who are more educated, independent, and long-lived than any before them. Yet, this newfound autonomy comes with significant systemic challenges, as these women navigate a world largely designed for traditional two-person households. A landmark report from the Harvard Joint Center for Housing Studies (JCHS), released today, casts a stark light on one of the most pressing issues: older women are now 37% more likely than men to face a severe housing cost burden. This disparity is not merely a personal budgeting dilemma but a confluence of factors including the pervasive "Singles Tax," a lifetime of lower earnings, and extended life expectancies. To move beyond merely "getting by," solo aging women in 2026 must adopt a strategy of "total sovereignty," meticulously planning across financial, health, and legal domains to ensure their continued independence and well-being.

The Rise of the Solo Aging Woman: A Demographic Shift

The increasing prevalence of solo aging among women is a culmination of several intertwined demographic and societal trends spanning the last half-century. Historically, women have outlived men, a biological advantage that has only become more pronounced with advances in healthcare and living standards. The average life expectancy for women in many developed nations now exceeds that of men by several years, meaning a greater likelihood of spending later life alone due to widowhood. Beyond biology, societal shifts have played a crucial role. Marriage rates have declined, and divorce rates have remained significant, leading to a larger proportion of women entering their later years without a spouse. Furthermore, the women of 2026 represent generations that have increasingly prioritized education and career development, often delaying or opting out of marriage and child-rearing. This pursuit of independence, while empowering, has inadvertently positioned them to confront a social and economic infrastructure still largely oriented towards coupled living. The Harvard JCHS report underscores this reality, noting that of the 16 million older adults living alone, a staggering 10 million are women, highlighting a critical need for tailored support systems and policy adjustments.

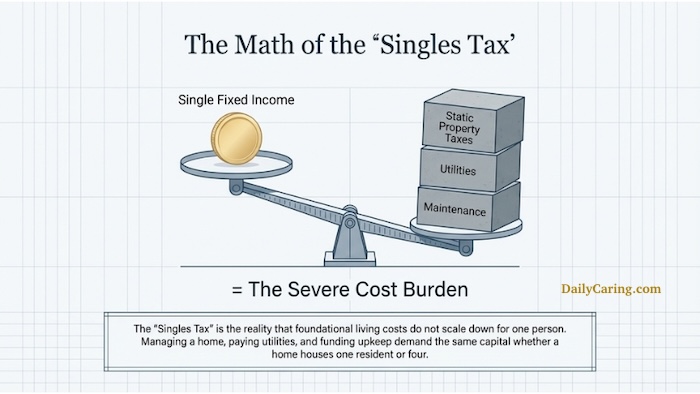

The "Singles Tax" and Financial Gravity: Unpacking the Economic Burden

The economic realities for solo aging women in 2026 are particularly harsh, exacerbated by what is colloquially known as the "Singles Tax." This isn’t just about paying full price for a hotel room or a single supplement on a cruise. It permeates daily life and significant expenditures. Property taxes, utilities, and home maintenance costs, for instance, remain largely constant whether a household comprises one person or four. This fixed cost burden disproportionately impacts single individuals who cannot share these expenses. The Harvard JCHS report’s finding that older women are 37% more likely than men to experience a severe housing cost burden—defined as spending more than 50% of income on housing—is a direct consequence of this "Singles Tax" combined with a lifetime of systemic financial disadvantages.

Women, on average, still earn less than men over their working lives, a gap that accumulates into significantly smaller retirement savings, pensions, and Social Security benefits. Data from organizations like the National Institute on Retirement Security consistently show women having lower average retirement account balances and receiving smaller pension payouts. This earnings disparity is compounded by career interruptions for caregiving responsibilities, which disproportionately fall on women. Consequently, many solo aging women enter retirement with fewer financial resources, making them highly vulnerable to inflation and unexpected expenses. The long-term implications are dire: reduced purchasing power, increased reliance on fixed incomes, and a heightened risk of poverty in old age. A 2023 AARP study, for example, highlighted that poverty rates among women over 65 living alone are significantly higher than those for older men living alone or for older couples. This financial gravity makes the goal of "total sovereignty" an uphill battle, requiring shrewd financial management and access to all available support.

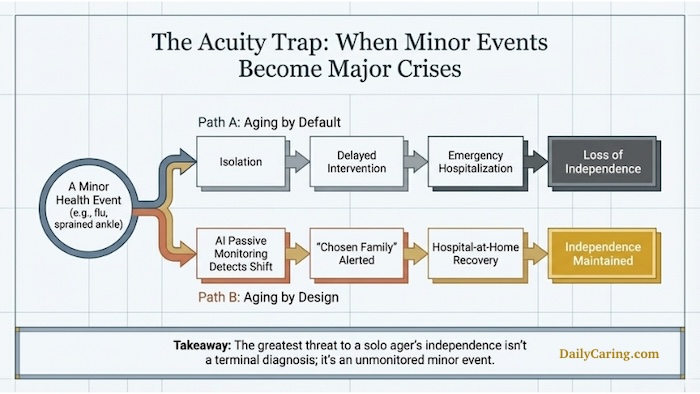

Healthcare Vulnerabilities: The "Acuity Trap"

Beyond financial pressures, solo aging women face unique challenges related to healthcare and personal safety, often referred to as the "acuity trap." For an individual living alone, a minor health event—such as a severe bout of the flu, a sprained ankle, or a fall—can rapidly escalate into a major crisis. Without an immediate family member or partner in the same household to provide basic assistance like fetching a glass of water, preparing a meal, or simply monitoring symptoms, recovery can be severely hampered. The absence of an informal caregiver network within the home places solo agers at a higher risk of delayed medical attention, prolonged recovery times, or even preventable complications that could lead to hospitalization or a permanent loss of independence.

The cost of professional in-home care, when needed, is prohibitively expensive for most, further deepening the vulnerability. The Genworth Cost of Care Survey consistently shows median annual costs for a home health aide ranging from tens of thousands of dollars, far exceeding the financial capacity of many solo aging women relying on limited retirement incomes. This creates a critical gap between the need for support during periods of acute illness or declining health and the ability to afford it. The psychological toll of this vulnerability cannot be overstated; the constant worry of falling ill or experiencing an accident without immediate help contributes to stress, anxiety, and an increased sense of isolation. This makes proactive health management, community engagement, and leveraging technological solutions paramount for solo aging women seeking to maintain their autonomy.

Navigating Legal and Administrative Complexities: The "Legal Lockout"

The path to "total sovereignty" for solo aging women also requires meticulous attention to legal and administrative preparedness, a domain where the absence of a traditional family structure can lead to a "legal lockout." Without a spouse or adult children readily available to step in during a crisis, managing financial accounts, healthcare decisions, and other personal affairs can become incredibly complex or even impossible if the individual becomes incapacitated. Basic tasks like accessing bank accounts, communicating with healthcare providers, or making urgent medical decisions require legal authority that must be established proactively.

The traditional system often assumes the presence of immediate family members to serve as proxies or agents. For solo agers, identifying and formally empowering a "Chosen Family" member—a trusted friend, a niece or nephew, or even a professional fiduciary—with digital power of attorney and healthcare directives is crucial. This ensures that someone has the legal standing to manage finances remotely, make informed medical choices, and oversee personal affairs should the need arise. Neglecting these preparations can lead to significant delays, financial mismanagement, and healthcare decisions being made by state-appointed guardians who may not fully understand the individual’s wishes or values. The growing complexity of digital assets, from online banking to social media accounts, further complicates matters, necessitating a comprehensive digital estate plan that outlines access and management protocols.

Strategies for "Total Sovereignty": Empowering Solo Agers

Achieving "total sovereignty" in 2026 requires a multi-faceted approach, integrating financial acumen, safety measures, and legal foresight.

-

Financial Fortification Against the Housing Squeeze: To counteract the disproportionate housing cost burden, solo aging women must proactively seek out financial relief. Programs like "Elderly Homeowner" property tax credits, which exist in many states and municipalities, can significantly reduce annual housing expenses. Local utility cost-sharing programs or energy assistance initiatives can also provide critical savings. Resources such as the National Council on Aging’s (NCOA) BenefitsCheckUp.org are invaluable tools, allowing individuals to identify and apply for federal, state, and local programs they may be eligible for, covering everything from medication costs to food assistance. Exploring alternative living arrangements, such as shared housing models or co-housing communities designed for older adults, can also offer both financial relief and built-in social support, although these require careful planning and compatibility.

-

Proactive Health and Safety with the "Acuity Trap" in Mind: Mitigating the risks associated with the "acuity trap" involves a blend of personal health management and technological integration. Regular preventative health check-ups are non-negotiable. For immediate safety, AI-driven passive monitoring systems are emerging as game-changers. These non-intrusive technologies can track daily routines, detect unusual activity (like a prolonged absence from a bed or bathroom), and notify a pre-selected "Chosen Family" network or emergency services in case of a potential health shift or fall. Wearable devices with fall detection capabilities and emergency call buttons also offer an immediate lifeline. The DailyCaring AI Caregiver Guide provides resources on how these technologies can be integrated into a solo ager’s life, offering peace of mind without compromising privacy.

-

Legal Preparedness for "Legal Lockout": Comprehensive legal planning is the bedrock of sovereignty. This includes establishing a robust Last Will and Testament, a Durable Power of Attorney for financial matters, and an Advance Directive for Healthcare (or Healthcare Proxy). Critically for solo agers, these documents must explicitly name trusted individuals within their "Chosen Family" who understand their wishes and are willing to act on their behalf. Given the digital nature of modern life, a detailed Digital Estate Plan, as outlined in DailyCaring’s Digital Estate Guide, is essential. This plan should catalog online accounts, passwords, and instructions for managing digital assets, from social media profiles to investment platforms, ensuring continuity and preventing "legal lockouts" in the digital realm.

Building Your "Chosen Family" Network: A Social Imperative

In 2026, the concept of "Chosen Family" is not merely a comforting idea but a critical component of a solo ager’s resilience strategy. For women without biological children or a spouse, this network of trusted friends, neighbors, and community members becomes their primary support system—a literal health insurance policy against the myriad challenges of aging alone. This network provides both practical assistance and vital emotional support, serving as a frontline defense against the pervasive "loneliness epidemic" that significantly impacts health outcomes.

The World Health Organization and other health bodies have increasingly recognized loneliness and social isolation as major public health concerns, comparable to smoking or obesity in their impact on morbidity and mortality. For solo agers, active cultivation of social connections is not a luxury but a necessity. This can involve formal structures, like joining retirement communities, co-housing initiatives, or senior centers, which offer built-in social engagement. It also encompasses informal relationships: the neighbor who holds a spare key, the friend with whom a daily text message check-in is routine, or a robust virtual community. These relationships provide practical help during minor health events, emotional solace, and a sense of belonging that is crucial for mental well-being. Building such a network requires intentional effort and reciprocal relationships, transforming casual acquaintances into a reliable web of mutual support.

Policy and Societal Implications: Adapting to a New Reality

The growing demographic of solo aging women presents significant policy and societal implications that demand proactive adaptation. Governments and policymakers must recognize that existing frameworks, often designed for traditional family units, are increasingly inadequate.

In terms of housing, there is a clear need for policy innovations beyond traditional subsidies. This could include incentivizing the development of smaller, more affordable housing units, promoting co-housing models through zoning reform, or expanding property tax relief programs specifically for low-income solo seniors. Social Security and pension systems may also require re-evaluation to better address the lifetime earnings gap faced by women, ensuring a more secure financial foundation for their later years.

Healthcare systems must also adapt to the unique needs of solo agers. This includes expanding access to affordable in-home care services, supporting community-based care networks, and integrating technology solutions like remote monitoring into mainstream care pathways. Public health campaigns could focus on combating loneliness and promoting social engagement among older adults, offering resources and platforms for community building.

Furthermore, a broader cultural shift is necessary. Society must move beyond outdated notions of what constitutes a "successful" or "supported" old age, embracing the diversity of living arrangements and acknowledging the strength and independence of solo aging women. This involves destigmatizing living alone and celebrating the "Chosen Family" model as a legitimate and vital support structure. Non-profit organizations and community groups play a crucial role in filling gaps, offering social programs, advocacy, and direct support services tailored to the needs of solo agers. Designing age-friendly cities and communities that prioritize walkability, public transportation, and accessible social spaces will also be critical in fostering environments where solo aging women can thrive.

Conclusion

Solo aging for women in 2026 is not about "doing it alone" in isolation, but rather about having the independent authority and agency to choose how, where, and with whom one lives. While the structural challenges highlighted by the Harvard JCHS report—from the financial burden of the "Singles Tax" to the vulnerabilities of the "acuity trap"—are undeniably real, the tools and strategies to overcome them have never been more accessible. From state-level financial relief programs and cutting-edge AI companions to the profound strength derived from a meticulously cultivated "Chosen Family," the pathways to "total sovereignty" are emerging. By recognizing these challenges and proactively building comprehensive plans today, solo aging women are not just protecting their futures; they are reclaiming their power, redefining what it means to age independently, and paving the way for a more inclusive and supportive society for generations to come.

{kind=link}