Significant Medicare Part D Reforms Take Full Effect in 2026, Capping Out-of-Pocket Prescription Costs and Eliminating the ‘Donut Hole’

Managing an older adult’s medications has historically represented a persistent and often unpredictable financial burden for millions of American families. Caregivers and beneficiaries have long navigated complex coverage phases, including the infamous "donut hole," which made accurate budgeting nearly impossible. The comprehensive Medicare Part D changes taking full effect in 2026, stemming from the landmark Inflation Reduction Act (IRA), are set to fundamentally alter this landscape, ushering in a new era of forced financial predictability for prescription drug costs under the federal program.

A New Era of Predictability: The Core 2026 Reforms

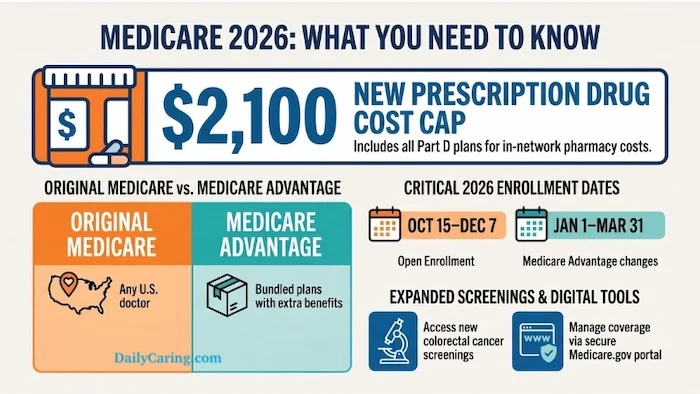

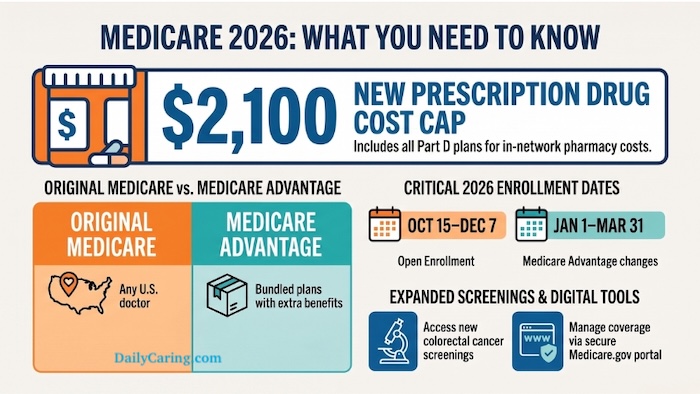

As of January 1, 2026, the final implementation phases of the Inflation Reduction Act will dramatically reshape how Medicare Part D beneficiaries pay for their prescription medications. The most significant change is the strict annual out-of-pocket (OOP) spending cap, legally set at $2,100. This means that once a Medicare Part D enrollee spends this amount out of their own pocket on covered prescription drugs within a calendar year, their plan or Medicare Advantage plan will cover 100% of the cost for all remaining covered medications for the rest of that year. Crucially, the maximum standard deductible for Part D plans is also legally set at $615 for the 2026 plan year.

This reform represents a monumental shift from the previous system, where beneficiaries could face unlimited costs in the catastrophic phase, albeit with significant plan contributions. Under the 2026 rules, once the $2,100 cap is reached, the patient’s cost drops to zero for covered drugs, with no exceptions and no lingering 5% coinsurance requirement in the catastrophic phase.

The Demise of the "Donut Hole": A Decade-Long Struggle Concludes

For over a decade, the "coverage gap," more commonly and ominously known as the "donut hole," stood as arguably the most financially destructive element of Medicare Part D for seniors. Introduced with the inception of Part D in 2006, this phase meant that once a beneficiary and their plan reached a specific spending threshold, their share of drug costs would suddenly spike, often requiring them to pay a substantial percentage of the drug’s price until they reached the "catastrophic" coverage level. This unpredictability created immense stress and financial hardship, particularly for those with chronic conditions requiring high-cost medications.

As of 2026, the donut hole is permanently eliminated. It no longer exists in any form. This crucial change, a cornerstone of the IRA, means beneficiaries will now transition directly from their initial coverage phase to the new $2,100 out-of-pocket cap, immediately followed by 100% plan coverage for the remainder of the year. This simplification is expected to provide substantial relief to the millions of beneficiaries who previously fell into the gap annually, many of whom struggled to afford their essential medications during this period. The end of the donut hole is not merely a technical adjustment but a profound improvement in the financial security and access to medication for Medicare enrollees.

The Genesis of Change: A Chronology of the Inflation Reduction Act’s Impact on Medicare

The 2026 reforms are the culmination of several phased implementations outlined in the Inflation Reduction Act, signed into law in August 2022. Understanding this timeline provides essential context for the current changes:

- 2023: Initial changes focused on insulin costs, capping out-of-pocket costs for a month’s supply of insulin at $35 for Part D beneficiaries. Additionally, adult vaccines recommended by the Advisory Committee on Immunization Practices (ACIP) became available with no cost-sharing under Part D.

- 2024: Significant changes were implemented in the catastrophic coverage phase. The 5% coinsurance requirement for beneficiaries in this phase was eliminated, meaning that once beneficiaries reached the catastrophic threshold (which was effectively $8,000 in total drug spending for 2024, including what the plan pays), they paid $0 for covered drugs for the rest of the year. The income limit for the Low-Income Subsidy (LIS), also known as "Extra Help," was expanded to 150% of the federal poverty level, offering more financial assistance to eligible low-income seniors.

- 2025: A cap on annual increases for Part D base plan premiums was introduced, limiting growth to 6% per year. This measure aimed to prevent insurers from simply offsetting new cost burdens by drastically increasing monthly premiums.

- 2026: This year marks the most impactful phase. The $2,100 out-of-pocket cap for covered Part D drugs takes full effect, completely eliminating the coverage gap (donut hole) and the 5% coinsurance in the catastrophic phase. This also initiates the Medicare Drug Price Negotiation Program, allowing Medicare to directly negotiate prices for a select number of high-cost prescription drugs, further aiming to reduce overall drug spending.

These phased changes demonstrate a deliberate legislative effort to incrementally reduce drug costs and improve financial stability for Medicare beneficiaries, with 2026 representing the pinnacle of these reforms regarding out-of-pocket spending limits.

The "Real Threat": Formulary Manipulation and the Imperative for Vigilance

While the new caps offer unprecedented financial protection, beneficiaries and their caregivers must remain highly vigilant. Insurance companies, as business entities, are not absorbing these new costs out of benevolence. Industry analysts and consumer advocates widely anticipate that insurers will aggressively manipulate their covered drug lists, known as formularies, and strategically shift medications into higher pricing tiers to offset these mandated caps and maintain profitability.

A drug that was fully covered or in a favorable tier in 2025 may be entirely dropped from a plan’s formulary in 2026, or moved to a higher tier with greater cost-sharing before the cap is met. This means that money spent on a drug not included in a plan’s formulary will not count toward the $2,100 out-of-pocket cap. This practice, while legal within certain regulatory bounds, places the onus squarely on beneficiaries to meticulously verify that their loved one’s specific medications remain on their chosen plan’s formulary during the Annual Enrollment Period (AEP).

Consumer advocacy groups, such as the Medicare Rights Center and the Kaiser Family Foundation, have consistently highlighted the importance of reviewing formularies, especially for beneficiaries with chronic conditions requiring specific medications. They warn that subtle changes in drug placement or coverage restrictions (like prior authorization or step therapy requirements) can significantly impact a patient’s access and effective cost, even with the new cap in place. Insurance companies, on their part, argue that such formulary management is essential to control overall plan costs, manage risk, and keep premiums affordable for all members. However, critics counter that these tactics can create new barriers to care.

Smoothing the Path: The Medicare Prescription Payment Plan

To further ease the financial strain, particularly for the initial deductible and early-year costs, the 2026 mandates also ensure the continuation of the Medicare Prescription Payment Plan. This innovative, opt-in program allows enrollees to smooth their out-of-pocket costs over the entire calendar year. Instead of facing a potentially large lump sum payment at the pharmacy counter, especially at the beginning of the year when deductibles are reset, caregivers can opt their loved one into this program. The pharmacy then bills the insurance plan, and the insurance plan sends the enrollee a manageable monthly bill for their share of costs, spreading the financial impact more evenly. This can be a significant benefit for managing household cash flow and preventing unexpected financial shocks.

Premium Stabilization: A Double-Edged Sword

Another critical, though less publicized, Medicare Part D change is the premium stabilization program. As of 2025, the law caps base premium increases at 6% per year. This measure was introduced to prevent insurers from simply jacking up monthly premiums to absorb the costs associated with the new out-of-pocket caps and the elimination of the donut hole. While this provides a degree of protection against runaway premium growth, it’s essential to understand that this cap applies to the base premium, not necessarily an individual plan’s premium. Individual plan premiums will still fluctuate based on a variety of factors, including the plan’s specific design, service area, and how it manages its overall costs. Therefore, annual comparison shopping remains absolutely critical to ensure beneficiaries are not overpaying for coverage or finding themselves in a plan that no longer meets their needs due to altered formularies.

Broader Implications and Stakeholder Reactions

The 2026 Medicare Part D reforms are expected to have wide-ranging implications across the healthcare ecosystem:

- For Beneficiaries and Caregivers: The most immediate impact will be enhanced financial predictability and a significant reduction in the financial burden for those requiring high-cost prescription drugs. This newfound stability can lead to better medication adherence, improved health outcomes, and reduced stress for caregivers. However, the increased complexity of formulary review means the "easy button" has not been pressed; active participation in AEP is more vital than ever.

- For Pharmaceutical Companies: The IRA’s broader provisions, including drug price negotiation which also begins in 2026, will exert significant pressure on pharmaceutical revenues. The out-of-pocket cap shifts some cost burden from patients to insurers, who in turn will likely intensify their pressure on manufacturers for rebates and discounts, and carefully manage formularies.

- For Insurance Companies: These changes present a significant operational and financial challenge. While premium stabilization offers some relief, the elimination of catastrophic phase coinsurance and the new OOP cap mean insurers are assuming greater financial risk for high-cost enrollees. This will drive more aggressive formulary management, tighter negotiations with drug manufacturers, and innovative plan designs to attract healthier members while managing costs for those with complex needs.

- For the Medicare Program and Policymakers: The reforms are hailed by proponents as a major step towards making prescription drugs more affordable and addressing a long-standing flaw in the Part D program. They underscore a shift towards greater government intervention in drug pricing and patient cost-sharing. Success will be measured not only by cost savings but also by improved patient access and health outcomes, and the prevention of excessive formulary restrictions.

Practical Guidance for Navigating the New Landscape

With these profound changes, proactive engagement during the Medicare Annual Enrollment Period (October 15 to December 7) is no longer optional; it is essential. Here’s what beneficiaries and caregivers should prioritize:

- Review Formularies Meticulously: Do not assume your current coverage is safe. Obtain the proposed 2026 formulary for your current plan and any prospective new plans. Cross-reference every medication your loved one takes to ensure it is covered and understand its tier placement and any associated restrictions (e.g., prior authorization, step therapy).

- Compare Plans Annually: Utilize the official Medicare Plan Finder tool on Medicare.gov. This powerful resource allows you to input your loved one’s medications and compare total estimated annual costs (premiums, deductibles, copays) across all available plans in your area.

- Consider the Prescription Payment Plan: If managing upfront costs is a concern, investigate enrolling in the Medicare Prescription Payment Plan to spread expenses evenly throughout the year.

- Seek Expert Advice: Consult with a State Health Insurance Assistance Program (SHIP) counselor. These are free, unbiased resources available in every state to help beneficiaries understand their options. Independent Medicare brokers can also provide personalized guidance, though it’s important to understand how they are compensated.

- Understand Total Costs: Factor in not just the $2,100 cap, but also the monthly premiums and the initial deductible. While the cap offers peace of mind for high spenders, lower premiums or deductibles can still save money for those who don’t anticipate hitting the cap.

The 2026 Medicare Part D reforms represent a significant legislative achievement aimed at bringing much-needed financial relief to millions of older adults and their caregivers. By eliminating the dreaded donut hole and capping out-of-pocket costs, the Inflation Reduction Act has laid the groundwork for a more predictable and equitable prescription drug benefit. However, the onus remains on beneficiaries to be informed, proactive, and diligent in reviewing their coverage options to fully leverage these changes and protect their access to essential medications.

| Medicare Policy Area | 2026 Update Details (or more) Medicare Part D Changes 2026: What Seniors and Caregivers Need to Know

This comprehensive guide provides an in-depth analysis of the Medicare Part D changes taking effect in 2026, stemming from the Inflation Reduction Act. These reforms are designed to significantly alter the financial landscape for prescription drug costs, bringing greater predictability and relief to millions of older adults and their caregivers.

The Landscape Before 2026: A History of Medicare Part D Challenges

Medicare Part D was enacted as part of the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 and went into effect in 2006. Its creation aimed to provide prescription drug coverage to Medicare beneficiaries, addressing a significant gap in the original Medicare program. However, its initial design included complex phases that often led to unpredictable and burdensome out-of-pocket costs for seniors with chronic conditions and high medication needs.

The original structure of Part D typically involved:

- Deductible Phase: Beneficiaries paid 100% of their drug costs up to a certain amount.

- Initial Coverage Phase: After meeting the deductible, beneficiaries paid a copayment or coinsurance, and the plan covered the rest, up to an initial coverage limit.

- Coverage Gap (Donut Hole): Once the initial coverage limit was reached, beneficiaries entered the "donut hole," where they were responsible for a much larger percentage of their drug costs (e.g., 100% in early years, later reduced to 25% for brand and generic drugs due to the Affordable Care Act). This phase was notorious for its financial unpredictability and the sudden spike in costs.

- Catastrophic Coverage Phase: After spending a certain amount out-of-pocket (which included money spent in the deductible, initial coverage, and donut hole phases), beneficiaries entered catastrophic coverage, where Medicare paid a large portion of the drug cost, but beneficiaries were still responsible for a 5% coinsurance, with no upper limit.

This 5% coinsurance in the catastrophic phase, despite covering a smaller percentage, could still amount to thousands of dollars annually for those on very high-cost specialty drugs, especially for conditions like cancer, multiple sclerosis, or certain rare diseases. This lack of an out-of-pocket maximum was a persistent point of contention and a source of significant financial stress for many families.

The Transformative 2026 Medicare Part D Changes: A Detailed Look

The Inflation Reduction Act (IRA), signed into law in August 2022, initiated a series of reforms designed to lower prescription drug costs for Medicare beneficiaries. The 2026 changes represent the most significant culmination of these efforts, fundamentally restructuring the Part D benefit design.

1. The Landmark $2,100 Out-of-Pocket Cap:

Beginning January 1, 2026, all Medicare Part D enrollees will benefit from a strict annual out-of-pocket spending limit of $2,100. This cap applies to all covered prescription drugs under their specific Part D or Medicare Advantage plan. Once a beneficiary’s total out-of-pocket spending—including their deductible, copayments, and coinsurance—reaches $2,100 within a calendar year, they will pay nothing for any further covered prescription drugs for the remainder of that year.

- Impact: This is a monumental change. Previously, beneficiaries in the catastrophic phase still paid 5% coinsurance, which for very expensive drugs could translate into tens of thousands of dollars annually. For example, a drug costing $10,000 per month would incur a $500 monthly coinsurance in the catastrophic phase, or $6,000 annually. Under the new system, once the $2,100 cap is hit, these costs drop to zero. This provides unprecedented financial predictability and protection against catastrophic drug costs, a benefit long sought by patient advocacy groups. An estimated 1.5 million Medicare beneficiaries annually spent more than $2,000 out-of-pocket on prescription drugs prior to these reforms, and this number is expected to grow. The cap directly addresses this vulnerability.

2. Elimination of the Coverage Gap ("Donut Hole"):

The notorious "donut hole" is officially and permanently closed as of 2026. This means beneficiaries will no longer face a period of significantly higher cost-sharing after their initial coverage limit is met. Instead, they will seamlessly transition from the initial coverage phase directly to the new $2,100 out-of-pocket cap.

- Impact: This simplifies the Part D benefit structure dramatically. The unpredictable nature of the donut hole often led to beneficiaries rationing medication or abandoning prescriptions due to sudden cost spikes. Its elimination removes a major barrier to medication adherence and provides a much clearer understanding of annual drug costs.

3. Standard Deductible Set at $615:

For the 2026 plan year, the maximum standard deductible for Medicare Part D is legally set at $615. This is the amount beneficiaries must pay out-of-pocket for covered prescription drugs before their plan begins to pay.

- Impact: While still an upfront cost, knowing this fixed amount allows for better financial planning. The deductible counts towards the $2,100 out-of-pocket cap, meaning it contributes to reaching the point where drug costs drop to zero.

4. The Medicare Prescription Payment Plan:

Introduced as an option in 2025 and continuing in 2026, the Medicare Prescription Payment Plan is an opt-in program designed to help beneficiaries manage their out-of-pocket costs more evenly throughout the year. Instead of paying large lump sums for their deductible and copayments at the pharmacy counter, enrollees can choose to spread these costs into predictable monthly payments.

- Impact: This plan offers significant cash flow benefits, especially for those who hit their deductible early in the year or have high initial copayments. By smoothing out expenses, it can prevent financial strain and make it easier for beneficiaries to afford their medications consistently. It’s particularly beneficial for individuals on a fixed income who need to budget carefully.

5. Premium Stabilization Measures:

As part of the IRA, a measure to cap annual increases in Medicare Part D base plan premiums at 6% was implemented in 2025. This aims to prevent insurers from simply raising monthly premiums excessively to offset the new out-of-pocket caps and other cost-sharing reductions.

- Impact: While this cap applies to the base premium, individual plan premiums can still fluctuate based on a variety of factors. This means that while overall premium growth for Part D plans is constrained, beneficiaries must still actively compare plans during the Annual Enrollment Period (AEP) to find the most cost-effective option for their specific needs. It’s a protection against broad market inflation but doesn’t eliminate the need for diligent comparison shopping.

The Unseen Challenge: Formulary Manipulation by Insurers

While the new caps and benefit structure offer substantial advantages, they also create new incentives for insurance companies. Since insurers are now responsible for 100% of covered drug costs after the $2,100 cap, they are expected to become even more aggressive in managing their formularies (the list of drugs they cover).

- Shifting Tiers: Insurers may move more drugs to higher cost-sharing tiers, increasing the amount beneficiaries pay out-of-pocket before reaching the $2,100 cap.

- Removing Drugs: Certain drugs, especially expensive brand-name medications where generic alternatives exist, might be removed from formularies entirely. If a drug is not on a plan’s formulary, the money spent on it does not count towards the $2,100 cap, and the beneficiary bears the full cost.

- Increased Restrictions: Plans may implement or expand prior authorization requirements (requiring doctor approval before coverage) or step therapy (requiring patients to try less expensive drugs first).

- Narrow Networks: Some plans might limit the pharmacies where beneficiaries can fill prescriptions, potentially restricting access or convenience.

Statements and Reactions from Related Parties:

- Patient Advocacy Groups (e.g., AARP, National Council on Aging): These groups have largely applauded the 2026 changes, particularly the $2,100 out-of-pocket cap and the elimination of the donut hole, as historic victories for seniors. They emphasize the relief this will bring to millions struggling with high drug costs. However, they also issue strong warnings about formulary manipulation, urging beneficiaries to be exceptionally diligent during AEP. They will likely push for greater transparency and oversight of insurance company practices.

- Insurance Companies (e.g., AHIP – America’s Health Insurance Plans): Insurers acknowledge the new regulations but express concerns about the financial impact on their plans. They argue that these mandates necessitate careful management of costs to maintain plan viability and keep premiums affordable for all members. Their public statements often highlight their commitment to providing access to affordable care while also emphasizing

{kind=link}