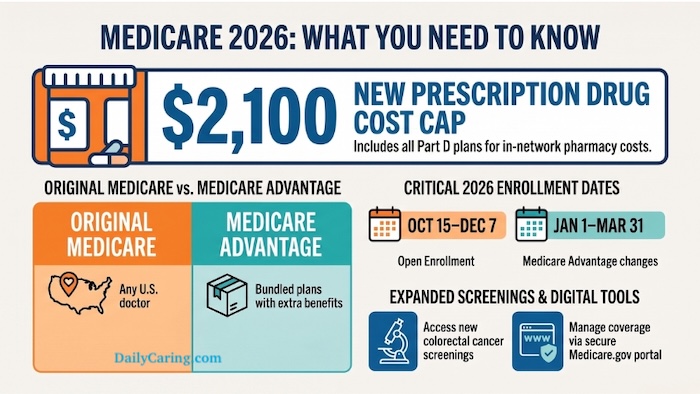

Medicare Part D Undergoes Historic Transformation in 2026: Out-of-Pocket Prescription Drug Costs Capped at $2,100, Eliminating the ‘Donut Hole’.

The landscape of prescription drug coverage for millions of American seniors is set for a monumental shift in 2026, as the final phases of the Inflation Reduction Act (IRA) of 2022 fundamentally reshape Medicare Part D. Caregivers and older adults, long burdened by the unpredictable and often exorbitant costs of essential medications, can now anticipate unprecedented financial predictability and relief. At the heart of these reforms is a strict annual cap on out-of-pocket prescription drug spending, set at $2,100, alongside the permanent elimination of the much-dreaded "donut hole" coverage gap. This pivotal change is poised to alleviate a persistent financial drain that has historically made budgeting for senior healthcare a complex and often distressing endeavor.

The Legislative Catalyst: The Inflation Reduction Act of 2022

The sweeping reforms taking effect in 2026 are the culmination of provisions within the Inflation Reduction Act, a landmark piece of legislation signed into law in August 2022. While the IRA addressed a wide array of policy areas, a significant portion was dedicated to lowering healthcare costs, particularly prescription drug prices, for Medicare beneficiaries. The Act’s intent was to empower Medicare to negotiate drug prices, cap insulin costs, and redesign Part D to provide greater financial protection against high out-of-pocket expenses. This comprehensive approach aimed to address long-standing criticisms of the Medicare Part D program, which, despite its benefits, often left beneficiaries vulnerable to spiraling costs once they reached certain spending thresholds. The reforms represent a concerted effort by policymakers to shift a greater share of the financial burden for high-cost drugs from individuals to insurance plans and, ultimately, pharmaceutical manufacturers.

A Phased Approach: IRA’s Drug Cost Reforms Timeline

The full impact of the Inflation Reduction Act on Medicare Part D has been rolled out in stages, demonstrating a deliberate legislative strategy to introduce significant changes without immediately overwhelming the healthcare system.

- 2023: Marked the initial phase, with a crucial cap of $35 on monthly out-of-pocket costs for insulin for Medicare beneficiaries. Additionally, recommended adult vaccines became free, removing a significant barrier to preventive care.

- 2024: Brought further relief by eliminating the 5% coinsurance requirement in the catastrophic phase of Part D. This meant that once beneficiaries reached the catastrophic threshold, they no longer had to pay a percentage of their drug costs, though they still faced a significant initial coverage gap. This year also saw the implementation of a penalty for drug companies that raise prices faster than inflation, a measure designed to curb escalating costs.

- 2025: Introduced a cap on the annual growth of the base Medicare Part D premium at 6%. This measure aimed to provide some stability to monthly premium costs, protecting beneficiaries from dramatic year-over-year increases.

- 2026: Represents the final and arguably most impactful phase of the IRA’s Part D reforms. This year sees the implementation of the $2,100 out-of-pocket cap, the complete elimination of the "donut hole," and the establishment of the Medicare Prescription Payment Plan, offering beneficiaries greater flexibility in managing their drug expenses.

Dismantling the ‘Donut Hole’: A Decade of Financial Strain Ends

For over a decade, the "donut hole," or coverage gap, was arguably the most financially devastating element of Medicare Part D for seniors and their families. Introduced with the inception of Part D in 2006, this phase meant that once a beneficiary and their plan had spent a certain amount on covered drugs (the initial coverage limit), the beneficiary would suddenly become responsible for a substantial percentage of their drug costs – historically 25% for brand-name drugs and 25% for generics after manufacturer discounts – until they reached a much higher "catastrophic coverage" threshold. This gap created immense financial uncertainty, forcing many seniors to choose between essential medications and other basic necessities. Many beneficiaries would find themselves unexpectedly facing thousands of dollars in drug costs within a calendar year, making it nearly impossible for families to budget effectively. The psychological toll of this unpredictability, coupled with the real financial hardship, often led to medication non-adherence, compromising health outcomes. As of 2026, this dreaded coverage gap is permanently eliminated, marking a profound victory for senior health advocacy and financial security. Beneficiaries will now transition directly from the initial coverage phase to a $0 out-of-pocket cost once the $2,100 annual cap is met.

Key Pillars of the 2026 Medicare Part D Overhaul

The 2026 changes are multifaceted, creating a new framework for prescription drug coverage under Medicare Part D:

- Strict Annual Out-of-Pocket Cap: The most significant change is the establishment of a $2,100 annual maximum on out-of-pocket spending for covered prescription drugs. Once an enrollee reaches this threshold within a calendar year, their Part D plan or Medicare Advantage plan will cover 100% of the cost of all covered medications for the remainder of that year. This eliminates the 5% coinsurance that previously applied even in the catastrophic phase, effectively bringing a beneficiary’s cost to zero.

- Standard Deductible Set at $615: For the 2026 plan year, the maximum standard deductible for Medicare Part D is legally set at $615. This is the amount a beneficiary must pay out-of-pocket before their plan begins to pay for covered drugs. It’s crucial to remember that many plans offer lower deductibles or even no deductibles for certain tiers of drugs.

- Elimination of the Coverage Gap (Donut Hole): As detailed, the coverage gap is permanently gone. There is no longer a phase where beneficiaries are responsible for a higher percentage of their drug costs after reaching the initial coverage limit and before catastrophic coverage.

- Medicare Prescription Payment Plan (MPPP): To prevent seniors from facing a large, immediate deductible hit at the beginning of the year, or significant costs before reaching the cap, 2026 mandates the continuation of the Medicare Prescription Payment Plan. This opt-in program allows enrollees to smooth their out-of-pocket costs, including the deductible and copayments, over the calendar year. Instead of paying a lump sum at the pharmacy counter, the pharmacy bills the insurance plan, and the plan sends the enrollee a monthly bill for their share of the costs. This provides crucial flexibility for budgeting.

- Premium Stabilization: While individual plan premiums will continue to vary, the law caps increases in the base Part D premium at 6% per year. This measure is designed to prevent insurers from simply offsetting the new out-of-pocket caps by significantly hiking monthly premiums.

Understanding the New Financial Landscape: Deductibles and Caps

The interaction between the standard deductible and the out-of-pocket cap is critical for beneficiaries to understand. In 2026, the maximum standard deductible is $615. This means that, for most plans, beneficiaries will pay the full cost of their covered medications until they have spent $615. After meeting the deductible, they will enter the initial coverage phase, where they pay a co-payment or co-insurance, and their plan pays the rest. This continues until their total out-of-pocket spending (including the deductible, co-pays, and co-insurance) reaches the $2,100 cap. Once that $2,100 threshold is met, the beneficiary pays $0 for all covered medications for the remainder of the calendar year. This structure introduces an unprecedented level of financial certainty, allowing families to forecast their maximum annual drug expenses with precision.

The Medicare Prescription Payment Plan: Smoothing Costs

The Medicare Prescription Payment Plan (MPPP), while optional, is a significant tool for managing the financial impact of prescription drugs. For a senior taking multiple expensive medications, reaching the $615 deductible early in the year could still represent a substantial immediate cost. The MPPP allows these costs to be spread out. For example, if a beneficiary expects to hit the $2,100 cap, they could opt to pay roughly $175 per month ($2,100 divided by 12 months), rather than potentially paying several hundred dollars in January, followed by varying amounts throughout the year. This voluntary program is designed to prevent "sticker shock" at the pharmacy and to make high initial costs more manageable, thereby improving medication adherence and reducing financial stress.

Beyond Out-of-Pocket: Premium Stabilization Measures

While the $2,100 out-of-pocket cap is a headline feature, the premium stabilization program, though less publicized, is equally vital for long-term affordability. The 6% annual cap on the increase of the base Medicare Part D premium aims to temper overall premium growth. Without such a measure, insurance companies might be inclined to significantly raise premiums to offset the increased costs they bear under the new out-of-pocket cap. However, it is crucial to understand that this cap applies to the base premium, not necessarily to individual plan premiums, which can still fluctuate based on plan design, benefits, and geographic area. This distinction underscores the continued importance of diligent annual comparison shopping during the Medicare Annual Enrollment Period (AEP).

The Unseen Battleground: Formulary Manipulation by Insurers

While the 2026 changes bring immense relief, a critical caveat remains: insurance companies are not absorbing these new costs out of altruism. Industry analysts and consumer advocates widely anticipate that insurers will aggressively manipulate their covered drug lists, known as formularies, and shift medications into higher pricing tiers to offset the mandated caps. A drug that was fully covered and affordable in 2025 may be dropped entirely from a plan’s formulary in 2026, or moved to a tier with higher co-pays, making it less accessible or more expensive until the cap is met. This practice allows insurers to manage their financial exposure while technically complying with the new regulations. Therefore, beneficiaries and their caregivers must meticulously verify that all necessary medications remain on their chosen plan’s formulary during the Annual Enrollment Period. If a prescribed drug is not on the formulary, money spent on it will not count toward the $2,100 out-of-pocket cap, nor will it be covered by the plan. This makes the Annual Enrollment Period (typically October 15 to December 7) more critical than ever before.

Expert Perspectives and Stakeholder Reactions

The 2026 Medicare Part D reforms have elicited a range of reactions across the healthcare ecosystem.

- Beneficiary Advocacy Groups: Organizations like AARP have lauded the changes, particularly the elimination of the donut hole and the out-of-pocket cap, as a long-overdue victory for seniors. They emphasize the tangible financial relief and improved health outcomes expected from better medication adherence. However, they also issue strong warnings about formulary changes, urging beneficiaries to be vigilant.

- Government and CMS: Officials from the Centers for Medicare & Medicaid Services (CMS) have highlighted the consumer protection aspects of the IRA, emphasizing increased predictability and reduced financial burden. They frame the reforms as a significant step towards making prescription drugs more affordable and accessible.

- Insurance Providers: Publicly, insurance companies affirm their commitment to complying with federal mandates. Privately, many express concerns about the increased financial liability and the operational complexities of implementing the new structure. These concerns are a primary driver behind the anticipated formulary adjustments and strategic pricing decisions, as insurers seek to balance compliance with maintaining profitability.

- Pharmaceutical Industry: While the 2026 changes primarily impact how Medicare Part D plans operate and how beneficiaries pay, the broader context of the IRA includes provisions for Medicare drug price negotiation, which has been met with strong opposition from pharmaceutical manufacturers. They argue that such measures stifle innovation and reduce investment in research and development for new drugs. However, the out-of-pocket caps are seen as a direct response to the high list prices set by these companies.

Broader Implications for Seniors and Caregivers

The implications of these changes extend far beyond simple cost savings. For seniors, the predictability of a hard cap on drug costs can significantly reduce stress and improve mental well-being, allowing them to focus on their health rather than financial anxieties. It is expected to improve medication adherence, as fewer individuals will forgo or ration necessary prescriptions due to cost. For caregivers, the reforms simplify financial planning, making it easier to budget for a loved one’s healthcare needs without the constant fear of unexpected, crippling drug expenses. The new framework empowers caregivers to better advocate for their loved ones, knowing the maximum financial exposure. However, the onus is now on caregivers and beneficiaries to be proactive during the Annual Enrollment Period, scrutinizing plan changes and formularies to ensure continued coverage for essential medications.

Navigating the New Era: Essential Steps for Beneficiaries

To fully leverage the benefits of the 2026 Medicare Part D changes and mitigate potential risks, beneficiaries and their caregivers should take several proactive steps:

- Review Formularies Annually: This is paramount. Do not assume that a drug covered in 2025 will be covered in 2026. Meticulously check that all prescribed medications are on your chosen plan’s formulary for the upcoming year.

- Compare Plans During AEP: Even with premium stabilization, individual plan offerings, co-pays, and formularies will vary. Use the Annual Enrollment Period (October 15 – December 7) to compare all available plans in your area, utilizing tools like the official Medicare Plan Finder on Medicare.gov.

- Consider the Medicare Prescription Payment Plan: Evaluate if the MPPP would benefit your financial situation. If you anticipate high drug costs early in the year, spreading payments monthly could ease your budget.

- Understand Your Deductible and Co-pays: Familiarize yourself with the specifics of your chosen plan, including the deductible amount and co-payment structures for different drug tiers.

- Consult with Experts: Do not hesitate to consult with a qualified Medicare advisor, a State Health Insurance Assistance Program (SHIP) counselor, or a financial planner specializing in eldercare. These professionals can provide personalized guidance tailored to your specific medication needs and financial situation.

The 2026 Medicare Part D reforms represent a monumental shift towards greater financial protection and predictability for seniors. While these changes offer substantial relief and an end to the "donut hole" nightmare, they also introduce new complexities, particularly regarding formulary management by insurers. Vigilance, informed decision-making, and proactive engagement during the Annual Enrollment Period will be essential for beneficiaries and their caregivers to navigate this new era successfully and ensure access to affordable, life-sustaining medications.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute professional financial or legal advice. Always consult with a qualified Medicare advisor or financial planner regarding your specific situation.

{kind=link}