Medicare Part D Undergoes Landmark Transformation in 2026, Capping Out-of-Pocket Prescription Costs and Eliminating the ‘Donut Hole’

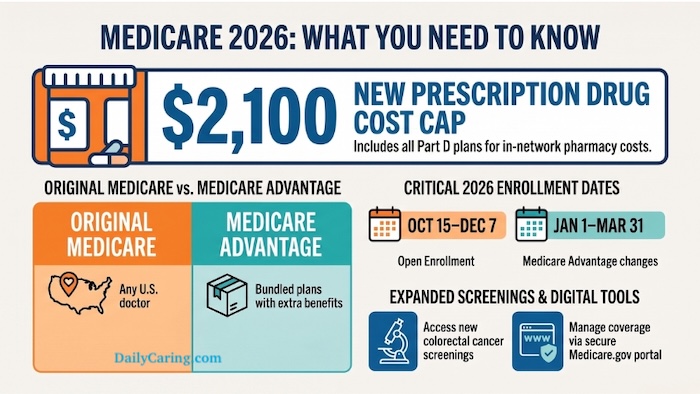

The landscape of prescription drug coverage for millions of older adults in the United States is set to undergo a profound transformation with the full implementation of the Inflation Reduction Act’s (IRA) Medicare Part D reforms in 2026. These changes, most notably the imposition of a strict $2,100 annual out-of-pocket cap on covered prescription drug costs and the permanent elimination of the infamous "donut hole," are poised to bring unprecedented financial predictability and relief to beneficiaries and their caregivers who have historically grappled with escalating and unpredictable medication expenses. Effective July 1, 2026, these mandates mark a significant shift in how Medicare Part D operates, aiming to mitigate the persistent financial drain associated with managing an older adult’s medications.

A New Era of Predictability: The 2026 Part D Reforms

For years, caregivers and seniors navigated a labyrinthine system of deductibles, initial coverage phases, the dreaded coverage gap, and catastrophic coverage, often leading to sudden and substantial out-of-pocket costs. The Medicare Part D changes for 2026 are designed to dismantle much of this complexity and volatility. Under the new regulations, the maximum annual out-of-pocket expenditure for covered prescription drugs is strictly capped at $2,100. This means that once an enrollee’s personal spending reaches this threshold within a calendar year, their Part D plan or Medicare Advantage plan will cover 100% of the cost of all subsequent covered medications for the remainder of that year. Crucially, there will be no 5% coinsurance in the catastrophic phase, effectively reducing the patient’s cost to zero after hitting the cap.

The standard deductible for Part D plans is also legally set at $615 for the 2026 plan year. While beneficiaries will still be responsible for this initial amount and subsequent copayments or coinsurance until they reach the $2,100 cap, the absolute ceiling provides a clear financial limit that was previously absent. This reform represents a monumental shift from the historical model, offering a level of budgeting certainty that has long been sought by those managing chronic conditions and multiple prescriptions.

The Demise of the ‘Donut Hole’: A Decade-Long Burden Lifted

Perhaps the most celebrated aspect of the 2026 reforms is the permanent eradication of the Medicare Part D coverage gap, widely known as the "donut hole." For over a decade, this phase represented a significant financial hurdle for seniors. After reaching a specific spending threshold in the initial coverage period, beneficiaries would suddenly become responsible for a substantial percentage of their drug costs – often 25% for brand-name and generic drugs – until they qualified for catastrophic coverage. This period of increased cost-sharing caught many off guard, leading to difficult choices between medication adherence and other essential living expenses.

The concept of the donut hole was introduced with the inception of Medicare Part D in 2006. It was initially designed as a mechanism to encourage beneficiaries to choose lower-cost generic drugs and to share in the cost of their medications. However, its practical effect was often devastating, plunging seniors into unexpected financial distress, particularly those with high medication needs or expensive specialty drugs. Data from organizations like the Kaiser Family Foundation consistently highlighted the financial strain the donut hole placed on millions of seniors annually, with many delaying or foregoing necessary prescriptions to avoid entering this costly phase. Its elimination in 2026, following gradual reductions in beneficiary responsibility over previous years, is a culmination of years of advocacy and legislative effort, ensuring a smoother transition from initial coverage directly to zero-cost catastrophic coverage.

The Legislative Journey: Inflation Reduction Act and its Phased Rollout

The Medicare Part D reforms are a direct result of the Inflation Reduction Act (IRA), signed into law in August 2022. While the IRA is a broad piece of legislation addressing climate change, healthcare costs, and tax reform, its provisions related to prescription drugs are among its most impactful. The act aimed to lower prescription drug costs for seniors through several key mechanisms, implemented in phases:

- 2023: Insulin costs for Medicare beneficiaries were capped at $35 per month per covered prescription. Vaccines recommended by the Advisory Committee on Immunization Practices (ACIP) became free for Part D enrollees.

- 2024: The 5% coinsurance requirement in the catastrophic phase of Part D was eliminated. This was a crucial precursor to the 2026 cap, as it removed the final layer of cost-sharing for the highest spenders.

- 2025: A $2,000 out-of-pocket cap for Part D covered drugs will be implemented, setting the stage for the final $2,100 cap in 2026. This cap also includes the initial deductible and copayments.

- 2026: The $2,100 out-of-pocket cap takes full effect, officially eliminating the coverage gap ("donut hole") and ensuring zero patient costs after the cap is met. This year also marks the beginning of the Medicare Prescription Payment Plan, offering beneficiaries the option to smooth out their out-of-pocket costs.

The journey to these reforms was long and often contentious, reflecting a decades-long debate over drug pricing and affordability in the United States. Patient advocacy groups, caregiver organizations, and many lawmakers consistently pushed for measures to rein in pharmaceutical costs, citing the disproportionate burden on seniors and those with chronic illnesses. The IRA’s passage represented a significant legislative victory for these efforts, promising substantial relief to millions of Americans.

Navigating the Nuances: Formulary Manipulation and Annual Enrollment

While the $2,100 cap offers significant financial protection, beneficiaries and caregivers must remain vigilant. Insurance companies are not absorbing these new costs without strategic adjustments. Industry analysts and healthcare policy experts anticipate that Part D plans will aggressively manipulate their covered drug lists, known as formularies, and shift medications into higher pricing tiers to offset the mandated caps. This means a drug that was fully covered in 2025 may be dropped entirely or moved to a more expensive tier in 2026.

This potential for formulary manipulation underscores the critical importance of the Annual Enrollment Period (AEP), typically running from October 15 to December 7 each year. During this time, beneficiaries must meticulously verify that their specific medications remain on their chosen plan’s formulary. If a drug is not on the formulary, the money spent on it will not count toward the $2,100 out-of-pocket cap, nor will it be covered by the plan. This necessitates proactive engagement from caregivers and seniors, reviewing plan documents, utilizing Medicare’s plan finder tools, and consulting with pharmacists or Medicare advisors to ensure continuous and affordable access to essential prescriptions.

The Medicare Prescription Payment Plan: Spreading Out Costs

To further alleviate the immediate financial strain on seniors, particularly at the beginning of the year when deductibles often apply, the 2026 reforms mandate the continuation of the Medicare Prescription Payment Plan. This opt-in program allows enrollees to smooth their out-of-pocket costs over the entire calendar year. Instead of facing a large lump sum payment for deductibles or high-cost medications at the pharmacy counter, participants can elect to pay their expected annual out-of-pocket costs in manageable monthly installments. The pharmacy bills the insurance plan, and the insurance plan then sends the enrollee a monthly bill for their portion. This program is particularly beneficial for those on fixed incomes, helping them budget more effectively and avoid unexpected financial shocks. It’s important to note that this plan is not mandatory; beneficiaries must proactively enroll if they wish to utilize this option.

Premium Stabilization: Guarding Against Excessive Hikes

Another vital, albeit less publicized, component of the Medicare Part D changes is the premium stabilization program. Recognizing that insurers might attempt to simply raise monthly premiums to cover the new out-of-pocket caps and other IRA provisions, the law caps base premium increases at 6% per year. This measure is intended to provide a degree of protection against exorbitant premium hikes that could undermine the affordability gains achieved through the out-of-pocket cap. However, it is crucial to understand that this cap applies to the base premium, which is an average across all plans. Individual plan premiums will still fluctuate based on various factors, including the plan’s specific benefit design, geographic location, and the formulary decisions made by the insurer. This again reinforces the necessity of annual comparison shopping and careful review of plan options to ensure the best value and coverage for individual needs.

Broader Implications: Impact on Stakeholders

The 2026 Medicare Part D reforms carry significant implications for various stakeholders across the healthcare ecosystem:

- Seniors and Caregivers: The most direct beneficiaries, experiencing reduced financial burden and increased predictability. This can lead to improved medication adherence, better health outcomes, and significant stress relief for families managing eldercare finances. It enables more effective long-term financial planning for healthcare costs.

- Pharmaceutical Companies: The industry has largely expressed concerns about the IRA’s provisions, particularly the drug price negotiation aspect (which fully phases in later, but is related to the overall push for lower costs). While the $2,100 cap directly impacts patient out-of-pocket costs, it shifts more financial responsibility to plans and, indirectly, to manufacturers through rebates and discounts. Pharmaceutical companies may adjust their pricing strategies for new drugs, increase research and development in specific therapeutic areas, or intensify lobbying efforts against future price controls.

- Insurance Providers (Part D Plans and Medicare Advantage Plans): These entities face a complex balancing act. They must absorb higher costs due to the out-of-pocket cap and the elimination of the donut hole, while adhering to premium stabilization rules. This will likely drive more aggressive formulary management, negotiations with drug manufacturers, and potential consolidation in the market. Plans will need to innovate in how they manage costs and attract beneficiaries.

- Healthcare System: The overall impact is expected to be positive for public health, as reduced financial barriers to medication access can lead to fewer hospitalizations and emergency room visits for preventable conditions. It could also influence prescribing patterns as physicians become more aware of patient cost-sharing.

Essential Action Steps for Caregivers and Beneficiaries

Given the scale of these changes, proactive engagement is paramount:

- Understand the New Caps: Familiarize yourself with the $2,100 out-of-pocket cap and the $615 deductible for 2026.

- Review Formularies Annually: During the Annual Enrollment Period (October 15 – December 7), meticulously check that all of your loved one’s prescribed medications are covered by their current or prospective Part D plan. Do not assume continuity.

- Consider the Medicare Prescription Payment Plan: Evaluate if enrolling in this opt-in program would benefit your budgeting by spreading out costs.

- Compare Plans: Use the official Medicare.gov plan finder tool to compare available Part D plans in your area, paying close attention to premiums, deductibles, formularies, and cost-sharing for specific drugs.

- Seek Expert Advice: Consult with a qualified Medicare advisor, SHIP (State Health Insurance Assistance Program) counselor, or financial planner to navigate the complexities and make informed decisions tailored to your specific situation.

The year 2026 marks a watershed moment for Medicare Part D, promising significant relief from the unpredictable and often overwhelming burden of prescription drug costs. While the new framework offers substantial benefits, it simultaneously places a renewed emphasis on active plan management and informed decision-making by beneficiaries and their caregivers to fully leverage these historic reforms.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute professional financial or legal advice. Always consult with a qualified Medicare advisor or financial planner regarding your specific situation.

{kind=link}